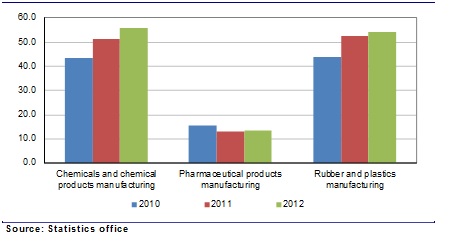

The Polish chemical sector recorded positive annual performance across all major segments in 2012, but the growth pace decelerated visibly compared to the previous year, in line with the slowdown of country’s economy and external demand. The situation is also partly due to high base comparison, particularly in the case of exports, which neared pre-crisis levels in 2011.

The growth of sales revenues in the chemical industry also eased visibly in 2012, to 5.6% y/y, from 10.5% y/y in 2011. Although the top chemical players reported rising y/y revenues in 2012, profitability deteriorated visibly following increase in raw material, natural gas and electricity. According to market data, 17 of the top 20 chemical players recorded y/y increase of revenues in 2012. In terms of net profit, however, more than half of them reported declining annual result.

Despite the slowdown of growth in 2012 and Jan-Apr 2013, the performance of the Polish chemical sector remains above the European average, where production contracted by 1.5% y/y in 2012 and by 2.1% y/y in Q1/2013.

Figure 1 Net sales revenues of chemical companies in 2010-2012 (annual, PLN bn)

These are only a few of the insights in the new Intellinews Report : Polish ChemicalSector. Learn more >>

Tags: Azoty, BASF, chemical, Ciech, companies, exports, Goodyear, government, M&A, Miraculum, output, PCC Exol, Poland, Polpharma, processing, production, PVC, sale, Solvay, Synthos, tyre, Unilever, ZCh Police

The IT market value maintained a positive annual performance across all major segments namely hardware, software and services in 2012.

Though the pace decelerated visibly compared to 2011, the Polish IT market remains as one of the fastest growing market in the CEE region and is expected to continue recording robust increase in the coming years.

EU-funded IT projects are expected to be the main driver for the market’s development this year. Besides that, the demand coming from the enterprise sector (large companies and SMEs) also remains strong.

According to market estimates the e-commerce segment increased by nearly 23% y/y in 2012 and is forecasted to continue developing at an accelerated pace in 2013, above the projected 16.1% y/y European average.

The share of e-commerce in the country’s total retail sales is expected to rise to over 4% this year from 3.8% in 2012 and 3.1% in 2011.

Figure 1 IT market value in 2010-2013f (PLN bn, y/y)

This is just a quick glimpse into the Intellinews Report: Intellinews – Polish IT Sector

Tags: AB, ABC Data, Action, Allegro, Amazon, Asbis, Asseco, business, capacity CEE, climate, cloud computing, Comarch, communication, computer, Czerwona Torebka, data centre, distributor, e-commerce, equipment, exports, government, growth, Grupa Nokaut, hardware, ICT, information, internet, IT, Komputronik, market, media, ministry, online, Poland, Polish, products, Qumak, sales, segment, shopping, smartphones, software, spending, Syngnity, Tech Data, technology, TVN

The Polish retail market maintained an upward y/y path in 2012, though sales slowed down visibly in Q4. The situation varied across segments, but overall the increase of market value was supported by the expansion of the large retail chains, which managed to offset the downward impact of a sluggish demand upon sales per store by the network enlargement (higher volumes).

The prospects for this year remained optimistic, considering the record-high shopping center deliveries planned, even though consumer demand will likely continue to deteriorate, paralleling the projected slowdown of the country’s economy.

Figure 1 Retail sales index in 2007-2013 (monthly, y/y in %)

These are only a few of the insights in the new Intellinews Report : Polish Retail Sector. Learn more and purchase now>>

Tags: abc, Abra, Avans, Biedronka, Black Red, Carrefour, CCC, clothing, construction materials, cosmetics, DIY, E.Leclerc, electronics, Farmacol, footwear, Forte, GDP, Gino Rossi, Griffin Topco, growth, hypermarkets, Ikea, inflation, Jysk, Komputronik, LPP, Media Expert, Media-Saturn Holding, Monnari, NeoNet, Netto, Neuca, Pelion, pharma, Poland, Poles, Polomarket, Prochnik, Redan, retail, Rossman, sales, Spar, supermarkets, unemployment, Vistula, Wojas, Zabka

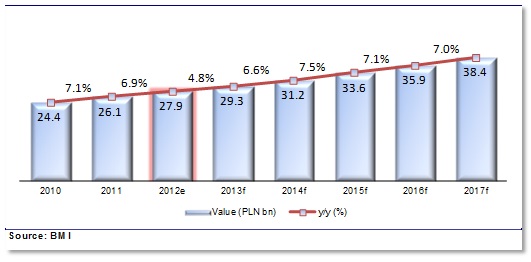

The Polish tourism industry benefited from the organisation of Euro 2012 championship last year. The number of foreign tourists visiting Poland in 2012 was the highest in five years, while the spending of foreign tourists reached the highest level since 2000. The total spending of foreign visitors in Poland during the Euro 2012 totaled PLN 1bn (EUR 247.7mn).

However, the effect of the sports event upon revenues in the tourism sector were not limited to boosting sales in June alone, but also rose the foreign visitors’ interest in Poland and extended the tourism season to September and October, thus allowing the sector to record higher revenues even in Q4.

In 2012, the total contribution of the travel and tourism sector to the GDP reached PLN 80.4bn (EUR 19.2bn), or 5% of GDP, up from PLN 75.9bn in 2011, according to estimates of the World Travel & Tourism Council.

Figure 1 Total contribution of travel&tourism to GDP in 2007-2013f (PLN bn)

Much more in the Intelinews report: Polish Tourism, Hotels & Restaurants Report

Tags: Accor, agencies, airports, AmRest, Bachleda Hotel, Capacity, catering, chain, Charley's, condohotels, DeSilva, developer, Domestic, Dominos Pizza, food, forecast, foreign, franchising, Gromada, Hilton, holiday, HoReCa, Hospitality, hotels, Infrastructure., investments, McDonald’s, Motel One, outbound, Poland, Polish, prices, restaurants, rooms, sector, Sfinks, spending, Subway, tourism, tourists, TRIPS

The construction and assembly index dropped by 1% y/y in 2012, marking a negative growth after the double-digit annual advance recorded in 2011. After a good performance in H1, the situation in the sector deteriorated abruptly in H2/2012 as infrastructure spending, the main growth driver in the past few years, was expected to fall with the completion of the main road building projects ahead of the Euro 2012 soccer championship.

The construction sector is expected to face challenges in 2013 and the coming years as well, particularly on the public building segment, but the outlook for the sector is not entirely gloomy, as the lowering demand from infrastructure can be replaced by alternatives in sectors such as rail and energy. However, overall the construction sector is expected to see visible recovery only in 2015, when EU co-financed projects for 2014-2020 are launched.

Figure 1 Constructions sector – Selective indicators in 2005-2012 (annual, y/y)

Much more in the Intelinews report: Polish Construction Sector

Tags: bankrupticy, Budimex, building, civil engineering, construction, economy, employment, energy, environment, gas, GDP, homes, Housing, Infrastructure., Insolvent PBG, M&A, office, oil, PBG, permits, Pol –Aqua, Poland, Polimex-Mostostal, Polish, rail, retail, sector, sentiment, Skanska, Strabag, Warbud, warehouse

The Polish automotive market was not resilient to the global economic crisis in 2012, when falling external and domestic demand impacted downward on output, domestic sales and exports. The production of passenger cars and light commercial vehicles dropped by 23% y/y in 2012 and the decline sharpened towards year end, as major producers downsized output in order to adjust to shrinking external demand, according to market data. Passenger car and LCV production further declined by over 22.7% y/y in January 2013 and is expected to follow the same tendency this year, as demand in Western Europe continues shrinking.

Since the Polish automotive sector is export-oriented, the prospects for the future are linked to developments in European markets. On the upside, as demand from its main partners, Germany and UK, is less vulnerable to abrupt changes, the Polish market remains stable and continues to attract investments in the sector.

Figure 1 Motor vehicle production in 2002-2012 (thou units, annually)

Figure 2 Production of passenger cars in 2008-2012 (thou pieces, annually)

Much more in the Intellinews report: Polish Automotive Sector

Tags: AB Volvo, auto, automotive, bus, car, components, Debica SA, demand, Domestic, economy, exports, Fiat Auto Poland, Fota, fuel, Goodyear, imports, industry, InterCars, LPG, market, Poland, Polish, producer, production, productivity, registrations, sales, tax, truck, tyre, vehicles, VW Motor Polska, VW Poznan, wages

As a whole, the banking sector across the CEE region remains profitable. Interest margins have tightened recently, but are still much higher than in Western Europe. Lending growth has softened and banks have increasingly focused on attracting fundings from domestic sources, increasing competition for deposits. Western European banks, which hold more than two thirds of the CEE banking sector’s assets, have withdrawn significant amounts of parent funding, pressured by heightened capital requirements in their home countries, but are believed to remain committed to the region, which has a strong growth potential. The main weakness of the CEE banking sector is the high level of bad loans and the trend for further worsening of the asset quality in view of the weak economic environment.

Much more in the Intellinews report: CEE Banking Sector Report

Tags: Bank for Reconstruction and Development (EBRD), Bank of Lithuania, banking, banks, Bulgaria, CEE, clients, credit institutions, Croatia, Czech Republik, deposits, domestic deposit, domestic loan, Estonia, European Investment Bank, foreign corporations, GDP, Germany, Goldman Sachs, Hungary, Latvia, lending, Lithuania, macroeconomy, MFI loans, National Bank of Poland (NBP), nn-performing loans, NPL ratio, Poland, Romania, Slovakia, Ukraine, UniCredit Bulbank

The Polish furniture market has not been completely resilient to the negative global economic developments and shrinking domestic and external demand. After a record year in 2011, when sold production of furniture, as well as exports, registered double-digit annual growth, the market slowed down visibly in 2012. The manufacturers adjusted to the declining demand, restructuring businesses and downsizing output.

Nonetheless, overall Polish companies managed to cope well with the shift in demand and stable profitability rates in the industry are relevant under these conditions.

The turnover profitability rate in the furniture industry in Jan-Sep 2012 remained at the same level as in full year 2011, namely 4.1%, according to official statistics. Prospects for the Polish furniture market remain optimistic, despite the expected slowdown in the short run. The sector remains attractive for foreign investors, who remain highly interested in acquiring or developing production facilities in Poland.

- Furniture industry- Net turnover, profitability rate in 2009-2012

Learn more from our Intellinews report: Polish Furniture Sector

Tags: Abra, Black Red White, distributor, exports, finance, foreign trade, Forte, Fritz Hansen, furniture, Griffin Topco, home furnishing, Ikea, IMS Sofa, industry, investment, Jysk, Mebelplast, Meble Emilia, Poland, price, producer, production, property, reatil, retailer, sales, stores, Swedsood, Swedspan

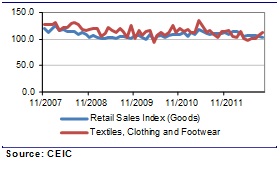

The Polish clothing and footwear market has been resilient to the global crisis so far. The retail segment registered positive performance in 2011 and remained on the same upward path in Jan-Sep 2012. The textile, clothing and footwear retail sales increased y/y every month over the period, except for May, when they dropped by 2.5% y/y. However, the performance of the market in the second half of the year is particularly important, as sales in H2 generate some 60% of the full-year total.

Despite the positive outlook, the clothing and footwear market has not remained completely unaffected by the economic slowdown and shrinking purchase power. The smaller players in particular faced with the negative effects of changing consumer behavior and buying pattern. Most of the large players, however, managed to report improving results y/y in Jan-Sep 2012 and plan further expansion of the chains. Furthermore, several new entries announced this year show that Poland continues to be attractive for international players not yet present on the market.

Figure 1 Retail sales index in 2007-2012 (monthly, y/y)

Much more in the Intellinews report: Polish Clothing and Footwear Industry

Much more in the Intellinews report: Polish Clothing and Footwear Industry

Tags: Bytom, clothing, export, footwear, foreign trade, Gino Rossi, import, KIK, LPP, Monnari, NG2, Poland, Prochnik, production, retailer, sales, shops, textile, Vistula, Wojas

The building materials market improved its performance within the construction industry in 2011, recovering from a two years decline from 2009 – 2010.

Nonetheless, as large infrastructure works neared completion ahead of the Euro 2012 championship, the consumption of construction materials also reduced in tandem. Official statistics show that output of most building materials witnessed annual decline in Jan-Sep 2012 and chances are that full-year performance will also be on the negative side.

Considering the high comparison base, the decrease is however not worrying and players expect the demand previously coming from large road infrastructure projects to be replaced by works in alternative areas, such as rail and energy.

In the short run, the industry will still face difficult times but market players have already redesigned strategies in order to cope with shrinking domestic demand.

")

Construction assembly production index in 2011-2012 (monthly, y/y)

Much more in the Intellinews report: Polish Construction Materials Sector >>

Tags: Armatura Krakow, Barlinek, bathroom, building materials, cement, Cemex, ceramic, Concrete, construction, construction chemicals, Etex, Ferrum, finance, fire safety systems, flooring, forecast, GDP, Gorazdze, growth, Grupa Ferro, Grupa Kety, investment, Lafarge, Lindab, LUG, market, materials, Megaron, Mercor, metal constructions, NewConnect, Nowa Gala, Pfleiderer Grajewo, plywood, Poland, Pozbud, price, production, residential, retail sales, revenue, sales, Selena, tiles, Tubadzin, Ulma Construccion Polska, wooden window

")